Azalea Apartments: Preserving Affordable Housing in Rural Bowling Green, Florida

In the rural town of Bowling Green, Florida, affordable rental housing is both scarce and critically important to the stability of the community. With a population of just over 2,400 people, the loss of even one affordable housing property in Bowling Green could have a lasting impact on the wellbeing of the property’s residents, and the community as a whole.

Azalea Apartments is a 40-unit housing development built in 1978. Supported by a HUD Housing Assistance Payment contract and spread across 20 small buildings, the property provides two, three, and four-bedroom apartments that are essential for families with low- and very-low incomes in Bowling Green. When Azalea’s longtime nonprofit owner decided to exit the Florida market, the property faced an uncertain future. Without a mission-driven buyer, the property risked leaving the U.S. Department of Agriculture (USDA) Section 515 program—threatening long-term affordability and housing stability for the families who call Azalea home.

Steven Brown, Executive Director of Florida Non-Profit Housing, Inc. (FNPH), says his organization was a natural fit to purchase the property. “We are a nonprofit in central Florida that has experience as a technical assistance provider to non-profits that built housing through the Rural Development 515 program, and the USDA 514/516 program for farmworkers,” Brown said. “We were committed to keeping the property affordable in perpetuity, and we were also interested in it because it was our first purchase of a USDA 515 property.”

.

How HAC Helped

By utilizing HAC’s Center for Multifamily Housing Preservation (the Center), FNPH was able to navigate the complex property transfer process and assemble the resources needed to preserve the property.

“The Center’s ability to assist non-profits and housing authorities is integral to keeping the 515 portfolio intact,” said HAC Rental Housing Development and Preservation Specialist Angela Shuckahosee. “Year after year, properties exit the portfolio as owners pay off their mortgages. Identifying capable, mission-driven non-profits and housing authorities who can become owners is the key to ensuring thousands of rural residents are not displaced and can maintain a rent payment that enables them to thrive instead of struggle.”

Early in the process, the Center provided hands-on technical assistance to FNPH, helping them evaluate the property’s finances, work through federal requirements, and plan for long-term stewardship. Recognizing that predevelopment funding is often a barrier for rural nonprofits, HAC’s loan fund also provided a 0% predevelopment loan that allowed the deal to move forward. As the transaction advanced, the Center supported FNPH through the USDA Rural Development transfer process and the assumption of the HUD Section 8 contract, ensuring rental assistance would remain in place for all 40 of Azalea’s units. When asked about their role in the transfer process, Brown made HAC and the Center’s importance clear:

“We would never been able to complete this transaction without the help of the dedicated HAC staff. Not only was their knowledge of the programs and process essential to moving the transfer to a successful conclusion, but their dedication to making the project successful in the long term was very advantageous to FNPH.”

The Result

Today, Azalea Apartments is positioned for long-term preservation as affordable housing in Bowling Green. The transfer to Florida Non-Profit Housing keeps the property in the USDA Section 515 program and preserves HUD rental assistance for every unit. As for their future plans, Brown indicated that FNPH hopes to obtain financing from USDA or another source to upgrade the apartments and offer homeownership counseling to residents who may want to move on and purchase a home.

For residents, this means stability—families can remain in their homes, and their community, without disruption. For FNPH, the project strengthens their organizational capacity and demonstrates how nonprofit ownership can protect affordability in challenging or underserved rural markets.

“We have added the preservation of existing low-income housing resources to FNLP’s mission, because we think it is vitally important for low-income families in rural areas,” Brown said. “We encourage other non-profit rural organizations to consider preserving this valuable resource in their communities.”

For the Center, Azalea Apartments reflects the power of early intervention, technical expertise, and mission-driven partnerships. As thousands of USDA Section 515 homes nationwide face similar risks, whether that means properties moving out of the 515 program, financial constraints, or other challenges present in rural America’s current housing landscape, preserving properties like Azalea helps ensure rural families continue to have safe, affordable places to live.

Housing Assistance Council

Housing Assistance Council

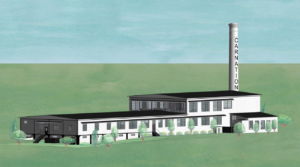

The Carnation Milk plant in Tupelo, Mississippi, has sat vacant since 1972. In about a year, that will change when 33 low-income senior households move into new affordable homes in this old factory. This May, Old Historic Carnation, LP broke ground on Carnation Village, a $16.8 million adaptive reuse project to convert the abandoned factory into 33 units of affordable senior housing. These units are sorely needed in Tupelo, a high-poverty community which needs over 1,500 additional senior affordable housing units. With a $325,000 loan from The Housing Assistance Council (HAC)—and two sixth-month extensions to that loan—the developer successfully navigated a predevelopment process mired in construction cost increases and unexpected funding gaps. Here’s how:

The Carnation Milk plant in Tupelo, Mississippi, has sat vacant since 1972. In about a year, that will change when 33 low-income senior households move into new affordable homes in this old factory. This May, Old Historic Carnation, LP broke ground on Carnation Village, a $16.8 million adaptive reuse project to convert the abandoned factory into 33 units of affordable senior housing. These units are sorely needed in Tupelo, a high-poverty community which needs over 1,500 additional senior affordable housing units. With a $325,000 loan from The Housing Assistance Council (HAC)—and two sixth-month extensions to that loan—the developer successfully navigated a predevelopment process mired in construction cost increases and unexpected funding gaps. Here’s how: The original project scope called for 50 units: 25 from an adaptive re-use of the plant itself and another 25 in a second building to be constructed next door. When our loan closed in July 2021, the project budget totaled about $12.7 million, to be funded by Low Income Housing Tax Credits, Historic Tax Credits, and a $1.6 million investment. Our financing covered the predevelopment costs of the work required to get to construction financing closing including environmental testing, historic preservation approvals, tax credit application and reservation fees, a market study, and an appraisal.

The original project scope called for 50 units: 25 from an adaptive re-use of the plant itself and another 25 in a second building to be constructed next door. When our loan closed in July 2021, the project budget totaled about $12.7 million, to be funded by Low Income Housing Tax Credits, Historic Tax Credits, and a $1.6 million investment. Our financing covered the predevelopment costs of the work required to get to construction financing closing including environmental testing, historic preservation approvals, tax credit application and reservation fees, a market study, and an appraisal.