State and local housing trust funds continue to offer flexible funding for affordable housing across the country, and a national fund has been created as well.

by Mary Brooks

This story appears in the 2015 Fall Edition of Rural Voices

This story appears in the 2015 Fall Edition of Rural Voices

Over the last 30 years of experience with housing trust funds, an amazing movement has been sustained and brightened by the tenacity and creativity of affordable housing/homeless advocates across this country. One could take a close look at almost any aspect of critical affordable housing needs in this country and see it being addressed within the housing trust fund community. The success of the housing trust fund movement offers undeniable evidence that we can provide everyone in this country with a safe affordable home. While the needs yet to be addressed are strikingly huge, if we committed the resources needed, we could end homelessness and provide safe affordable homes for all. It is an issue of resources and a challenge to the political will of this country.

State and local housing trust funds continue to offer flexible funding for affordable housing across the country, and a national fund has been created as well.

by Mary Brooks

This story appears in the 2015 Fall Edition of Rural Voices

Over the last 30 years of experience with housing trust funds, an amazing movement has been sustained and brightened by the tenacity and creativity of affordable housing/homeless advocates across this country. One could take a close look at almost any aspect of critical affordable housing needs in this country and see it being addressed within the housing trust fund community. The success of the housing trust fund movement offers undeniable evidence that we can provide everyone in this country with a safe affordable home. While the needs yet to be addressed are strikingly huge, if we committed the resources needed, we could end homelessness and provide safe affordable homes for all. It is an issue of resources and a challenge to the political will of this country.

More than 750 housing trust funds in cities, counties, and states throughout the United States are providing hundreds of millions of dollars to support needed safe affordable homes. Housing trust funds receive dedicated sources of public funds to provide an ongoing source of financing to support affordable housing for those most in need. A housing trust fund is typically established through a local ordinance or state law that creates the fund itself, identifies an administrative structure for overseeing its operation, establishes regulatory requirements for expenditure of the funds, and enables the dedication of identified sources of public funds.

Forty-seven states have created housing trust funds, although three of these have yet to commit revenue to the funds. While all state housing trust funds distribute funds across the state, at least Illinois, Kentucky, Nebraska, Nevada, Ohio, Oklahoma, Texas, Utah, and Washington either set aside a portion of available funds to be used specifically in rural areas of the state or are subject to a statutory target to do so.

Despite having dedicated public revenues, housing trust funds suffered greatly during the last recession. Committed revenue streams collected reduced amounts of money and, in several states, funds were used to patch budget deficits. Now all indications are that this is reversing, with several states renewing, if not building, their support for state housing trust funds. Just in the last year wins occurred in Connecticut, Florida, Hawaii, Minnesota, North Dakota, Ohio, Vermont, Virginia, Washington, and Washington, D.C. And several advances, including new housing trust funds, have been created at the local level.

State housing trust funds have learned how to brag about the affordable homes they have made possible throughout their states, including rural areas. There are lots of good reasons for this. First, it informs elected officials about the value of investing in affordable housing within the entire state, including the areas they represent. Second, it illustrates the importance of state funds supporting affordable housing and the flexibility these trust funds can provide, recognizing that affordable housing in different parts of the state may require different approaches. Third, it demonstrates what is possible – what can be accomplished if we commit the resources to make it work.

The single most commonly expressed advantage of creating local and state housing trust funds is the flexibility they provide in addressing a wide range of housing/homeless needs. Housing trust funds are designed to meet specific objectives, most often including serving those with the lowest incomes, ensuring long-term affordability, meeting accessibility and energy efficiency standards, and providing support throughout the state to all geographic areas. Yet, at the same time, they can also be called upon to meet unique challenges and take advantage of immediate opportunities.

The South Dakota Housing Opportunity Fund established a special application process to address the devastating impact of the Delmont tornado – a good example of how these flexible funds can be drawn to address unique, and in this instance urgent, circumstances. The simple application allows funds to be used for down payment assistance, home reconstruction, rental or utility deposits, or purchasing appliances.

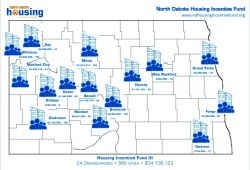

The illustrations here show how North Dakota and Ohio have made funds available across the state in a wide variety of geographic areas.

|

| NORTH DAKOTA’S HOUSING INVESTMENT FUND |

|

North Dakota’s Housing investment Fund is sustained through contributions in exchange for tax credits and funds from the Bank of North Dakota. The Fund has supported more than 2,000 affordable homes and averaged an additional $4 for every $1 invested by the fund. |

|

| THE OHIO HOUSING TRUST FUND |

|

The Ohio Housing Trust Fund is supported through revenues collected form document recording fees. Currently, the fund distributes grants and loans through these five programs:

- Target of Opportunity Grant Program

- Homeless Assistant Grant Program

- Housing Assistance Grant Program

- Housing Development Assistance Program

- Microenterprise Business Development Program

|

|

The Nebraska Housing Developers Association provides some insight into how the nonprofit and for-profit development communities have been integral to the success of the housing trust fund movement. “Nebraska uses its Housing Trust Fund to support development of rental housing in rural Nebraska,” explains Danielle Hill, Executive Director of the Association.

“The availability of rental housing in rural Nebraska is critical to the economic viability of many small communities. Other housing resources, such as the Low Income Housing Tax Credit, are not as efficient when fewer than 12 units are being developed. In many of Nebraska’s rural communities, contractor jobs and material supply companies are supported through the development and or rehabilitation of housing. This same development adds to the community’s tax base.”

The Nebraska Affordable Housing Trust Fund is statutorily required to allocate at least 30 percent of annual revenues to each of the state’s three congressional districts. Within its first ten years of operation, the Fund awarded nearly $88 million, which was matched with more than $300 million in other public and private funds. This helped support 4,765 affordable homes throughout the state and created at least 6,300 jobs.

The availability of rental housing in rural Nebraska is critical to the economic viability of many small communities.

Another promising advance in the housing trust fund field has occurred in states that have passed enabling legislation either encouraging the creation of local housing trust funds and/or making revenue options available to them. These state enabling programs vary across the country but the evidence indicates real impact across the states. Here are just a few examples.

Pennsylvania: Act 137 enabled counties to increase their document recording fees if the funds were committed to affordable housing activities. More than half the counties in the state have done so and funds are used to support a variety of activities from senior citizen housing to owner-occupied rehabilitation work to financial assistance for developing rental housing.

Florida: A majority of the funds in the Florida state housing trust fund support the State Housing Initiatives Partnership Program, allocating funds, based on a formula, to every county within the state and to entitlement cities.

Washington: The state passed legislation that increased the document recording fee and allocates these funds to each county to address homelessness.

Massachusetts: The Community Preservation Act has enabled more than 150 communities to enact a surcharge on real property taxes to create local dedicated funds for four purposes: affordable housing, open space preservation, historic preservation, and outdoor recreation. Creation of these funds also triggers annual distributions from the statewide Community Preservation Act Trust Fund, which derives its revenues from fees collected at the state registries of deeds.

Iowa: The Iowa Housing Trust Fund reserves at least 60 percent of its revenue for the local housing trust fund program, matching what local funds can generate throughout the state. At this point, 27 city, county, and regional local funds have been certified as eligible to receive matching state funds.

The housing trust fund movement’s strong history has enabled affordable housing/homeless advocates across the country to integrate new elements into statewide and local campaigns that are proving to be particularly effective.

First, many economic benefits of investment in affordable housing can be documented. The money housing trust funds commit to affordable housing activities leverages additional funds from other public and private sources, bringing additional revenues into communities. Studies across the country highlight the full range of economic benefits, including job creation, tax revenues, and more. Here are a few examples.

- The economic impact of Philadelphia’s trust fund is expected to reach nearly 2,600 jobs statewide each year, $80 million in wages every year, and increased city and state taxes.

- One-time construction activities from $10 million annual funding can inject $1 billion into the economy of Virginia between 2012 and 2022. The ongoing economic impact could reach $331 million per year, supporting 1,778 jobs throughout the state.

- A study for Lexington, KY concluded that more than 363 new jobs will be directly and indirectly supported from the implementation of the city’s trust fund and more than $43.3 million of direct, indirect, and induced economic activity will be generated.

- Within the first ten years of implementing the Alabama Housing Trust Fund, the total economic impact is estimated to equal $1.1 billion of output, creating or rehabilitating more than 7,100 homes, and generating 6,500 full-time jobs for Alabamians. The study estimates that the taxes collected at the state and local levels will be $151.5 million over the first ten years.

The second is the power of putting a face to the value of home. Numerous studies (many supported through the MacArthur Foundation’s How Housing Matters to Families and Communities initiative) have documented housing’s effects and the relationship between safe affordable homes and school performance, health benefits, environmental quality, and so much more. The stories individuals and families can share about how their lives are impacted when they secure affordable homes brings a powerful perspective to why these initiatives do matter. The Housing Assistance Council has recognized this for many years in sharing many of these stories in Rural Voices. Many campaigns and the affordable housing/homeless coalitions that wage them have incorporated videos, postcards, and stories to bring their messages home.

Recognizing the breadth of safe, affordable housing’s impact on communities has also brought into perspective just how housing does matter in terms of many related issues, including education, health, environment, employment, and much more. This has enabled many affordable housing/homeless coalitions to build cross-issue alliances integrating new and inspiring perspectives into the challenge of securing additional resources to meet the need for affordable housing.

Finally, a very exciting element of movement building is being considered in several states focused on the engagement of residents in affordable housing complexes, empowering them to bring their voices to affordable housing/homeless advocacy. These efforts could enable thousands to join these campaigns. From gathering postcards, to Twitter storms, to engaging in lobby days, hearing from those who have benefitted from the very affordable housing/homeless policy changes accomplished throughout the country is a striking statement of success and the promise of what we can do … when the will is there.

Mary Brooks works at the Housing Trust Fund Project of the Center for Community Change, housingtrustfundproject.org.

In fall 2003, we looked at a new self-help housing program on the Pine Ridge Indian Reservation, developed by the Oglala Sioux Tribe Partnership for Housing (OSTPH). We looked at what it took to create the program, some challenges to self-help housing on tribal trust land, and ingredients for success.

In fall 2003, we looked at a new self-help housing program on the Pine Ridge Indian Reservation, developed by the Oglala Sioux Tribe Partnership for Housing (OSTPH). We looked at what it took to create the program, some challenges to self-help housing on tribal trust land, and ingredients for success.