Rural Seed Money Loan Products

The Housing Assistance Council (HAC) operates several loan funds that provide vital seed money to rural housing developers: community-based, nonprofit organizations, housing development corporations, self help housing sponsors, farm worker organizations, cooperatives, Indian tribes, public agencies, units of local government, public utility districts, and small business and minority contractors. HAC funds help these organizations and individuals take the steps necessary to improve housing and living standards for rural, low- and very-low-income households, such as creation of subdivisions and new single- or multifamily housing units, rehabilitation of existing units, and improved water and waste water disposal systems in rural communities.

The Housing Assistance Council’s loan fund provides low-cost financing to developers of affordable housing in rural communities nationwide. Funds are currently available at 5.0% interest with a discounted 1.0% service fee; borrowers are responsible for closing costs. Current interest rate for for-profit developers is 8%. The standard loan term is three years. There is no maximum loan amount, although loans may not exceed available collateral. Loans must be recoverable from the permanent financing for the project.

Loans must be for projects, which include provisions for serving low-income people as defined by federal guidelines. Projects serving low- and very-low income persons will receive priority. At least 51% of the resulting housing units must be affordable to low- or very-low income people. The proposed projects must be located in areas that are rural in character and have populations of less than 25,000. Each of HAC’s loan products is briefly described below.

PRE-DEVELOPMENT

Loan funds are available for predevelopment expenses associated with the development of affordable housing. Eligible uses are: land options, down payments, architectural and engineering fees, site surveys, soil test borings, market studies, appraisals, environmental engineering studies, archeological clearances, and legal expenses related to site acquisition.

SITE ACQUISITION

Loan funds are available for acquisition and related costs for the development of affordable housing. Eligible uses are: land options, escrow payments, land purchase, legal expenses associated with site acquisition, and other reasonable closing costs.

SITE DEVELOPMENT

HAC loan funds may finance site development expenses associated with affordable single-family and multifamily development including self-help housing. Eligible expenses are: impact and permit fees, engineering surveys/fees, clearing and grading, wells, septic/water, sewer installation, utility hook-ups, streets, curbs, sidewalks, and legal expenses for site development.

CONSTRUCTION

Loan funds may finance unit construction costs of affordable housing developments. Eligible expenses are: construction materials and labor, construction bonds, construction inspection fees, legal costs, and title and recording fees. The maximum loan amount for construction loans is currently $750,000 and limited to single-family development. All fees incurred by HAC, including legal costs, hiring of a local construction inspector, title, and recording fees, will be charged to the borrower and, if necessary, financed by the HAC loan. The term of the loan will be determined by the needs of the project, pending underwriting review.

HAC’s SELF-HELP HOMEOWNERSHIP OPPORTUNITY PROGRAM (SHOP)

HAC provides loan funds through the HUD Self-Help Homeownership Opportunity Program (SHOP) to self-help housing providers for land acquisition and infrastructure improvement for the development of self-help units. The homebuyer family must contribute a significant amount of sweat-equity towards the construction of the dwelling. Loan funds are made available through a competitive application process and cannot exceed $15,000 per lot. SHOP loans are at 0% interest. Up to 90% of the SHOP loan may be forgiven when the borrower has satisfied the conditions of the loan agreement. The forgivable portion may become a grant for the group to establish its own revolving loan fund for future site acquisition and development of self-help housing or to provide direct subsidies to participating homebuyer families. SHOP funds are subject to HUD Environmental Review regulations.

PRESERVATION LOAN

PRLF proceeds are for short- or long-term costs of preservation, repayment and rehabilitation of USDA RHS Section 515 properties. Loans may be used for refinancing and costs incorporated into long-term financing such as options; downpayments; purchase; site development; architectural and engineering fees; construction financing; working capital and construction bonds; costs associated with USDA RHS required Capital Needs Assessments; preliminary easement and water rights purchase; legal expenses to establish utility districts; bonding; interim financing of local share costs; acquisition of existing private systems for rehabilitation; and emergency repair; and rehabilitation and repair.

If you are interested in applying for HAC loan funds, please contact HAC at (202) 842-8600, for information regarding application criteria and to request an application packet.

Applications should be submitted to HAC’s National Office at 1025 Vermont Avenue, N.W., Suite 606, Washington, D. C. 20005, Attention: Loan Fund Division. Telephone (202) 842-8600. Information about HAC and state and federal loan programs may be obtained from the same address or from the HAC Regional Offices.

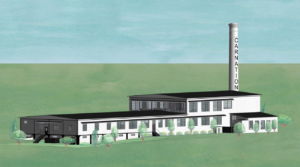

The Carnation Milk plant in Tupelo, Mississippi, has sat vacant since 1972. In about a year, that will change when 33 low-income senior households move into new affordable homes in this old factory. This May, Old Historic Carnation, LP broke ground on Carnation Village, a $16.8 million adaptive reuse project to convert the abandoned factory into 33 units of affordable senior housing. These units are sorely needed in Tupelo, a high-poverty community which needs over 1,500 additional senior affordable housing units. With a $325,000 loan from The Housing Assistance Council (HAC)—and two sixth-month extensions to that loan—the developer successfully navigated a predevelopment process mired in construction cost increases and unexpected funding gaps. Here’s how:

The Carnation Milk plant in Tupelo, Mississippi, has sat vacant since 1972. In about a year, that will change when 33 low-income senior households move into new affordable homes in this old factory. This May, Old Historic Carnation, LP broke ground on Carnation Village, a $16.8 million adaptive reuse project to convert the abandoned factory into 33 units of affordable senior housing. These units are sorely needed in Tupelo, a high-poverty community which needs over 1,500 additional senior affordable housing units. With a $325,000 loan from The Housing Assistance Council (HAC)—and two sixth-month extensions to that loan—the developer successfully navigated a predevelopment process mired in construction cost increases and unexpected funding gaps. Here’s how: The original project scope called for 50 units: 25 from an adaptive re-use of the plant itself and another 25 in a second building to be constructed next door. When our loan closed in July 2021, the project budget totaled about $12.7 million, to be funded by Low Income Housing Tax Credits, Historic Tax Credits, and a $1.6 million investment. Our financing covered the predevelopment costs of the work required to get to construction financing closing including environmental testing, historic preservation approvals, tax credit application and reservation fees, a market study, and an appraisal.

The original project scope called for 50 units: 25 from an adaptive re-use of the plant itself and another 25 in a second building to be constructed next door. When our loan closed in July 2021, the project budget totaled about $12.7 million, to be funded by Low Income Housing Tax Credits, Historic Tax Credits, and a $1.6 million investment. Our financing covered the predevelopment costs of the work required to get to construction financing closing including environmental testing, historic preservation approvals, tax credit application and reservation fees, a market study, and an appraisal.

Learning about the self-help program was a side benefit of Glenn’s participation in the training program. He suggested to his mom, Patsy Hayden that she should apply, since she has always wanted her own house. Glenn is delighted to be helping her make that dream reality — just in time for her fiftieth birthday.

Learning about the self-help program was a side benefit of Glenn’s participation in the training program. He suggested to his mom, Patsy Hayden that she should apply, since she has always wanted her own house. Glenn is delighted to be helping her make that dream reality — just in time for her fiftieth birthday.