Rural Voices: Making Choices

by Nick Mitchell-Bennett and Dr. Daniel Elkin

Innovations behind factory-built housing and the politics behind rural survival. Read the entire Rural Voices edition.

Making Choices_NMB

by Nick Mitchell-Bennett and Dr. Daniel Elkin

Innovations behind factory-built housing and the politics behind rural survival. Read the entire Rural Voices edition.

Making Choices_NMBby Congressman Bennie G. Thompson

This story appears in the 2015 Fall Edition of Rural Voices

This story appears in the 2015 Fall Edition of Rural Voices

Rural America is still a fundamental part of the fabric that holds this great nation together. Unfortunately, the pace of our economic growth and quality of life continue to lag behind those of our urban neighbors. People in rural America are still more likely to reside in substandard housing, receive inadequate education, and live in a community that is medically underserved.

by Congressman Bennie G. Thompson

This story appears in the 2015 Fall Edition of Rural Voices

Rural America is still a fundamental part of the fabric that holds this great nation together. Unfortunately, the pace of our economic growth and quality of life continue to lag behind those of our urban neighbors. People in rural America are still more likely to reside in substandard housing, receive inadequate education, and live in a community that is medically underserved.

Despite these challenges, people in rural America remain resilient and hopeful that better times are ahead. We, the federal government, can help them if we refocus our efforts to improve their quality of life through programs that have proved to be effective and economical.

With the current crazed obsession with reducing government programs dominating the narrative in Washington, it is more important than ever that we continue to vocalize the need for continued investment in affordable housing options in this country. Nowhere is this more important than in rural America where a quarter of our children live in poverty.

A look at some of our more successful programs shows that rural housing programs are under attack and need more advocates to fight for their survival. The Section 502 direct loan program is USDA’s flagship housing loan program and is designed to help low-income families purchase houses specifically in rural areas. Funds can be used to build, repair, or renovate a house, including providing water and sewage facilities. The program provides fixed-interest mortgage financing to low-income families who are unable to obtain credit elsewhere. The program also provides “supervised credit” including pre-loan and post-loan credit counseling to its borrowers to help them maintain their homes during financial crises. To date, this program has assisted more than two million families to increase their wealth by $40 billion. The program has seen a significant decline in enacted loan authorizations over the past decade, however. The fiscal year 2005 authorization was $1.14 billion. Today, the program is authorized at $900 million.

Unfortunately, the pinch doesn’t stop there. The Section 523 mutual self-help grant program allows low- and very low-income rural Americans to use “sweat equity” to reduce the costs of homeownership. Nonprofit organizations and local governments may obtain grant funds to enable them to provide technical assistance to groups of families that work cooperatively to build their houses. Typically, future homeowners use the aforementioned Section 502 direct loans to finance their mortgages and, through their own labor on constructing the houses, are able to reduce costs by 10-15 percent. This cherished program has seen its budget reduced from $34 million in fiscal year 2005 to $27.5 million in fiscal year 2015.

Rural rental housing is also at risk. USDA’s Section 515 loan program has not been able to fund any new rental units since 2011. The Section 521 Rental Assistance program, which helps low- and very low-income tenants pay their rent, ran out of funding in August or September 2015, leaving some landlords without reimbursement for the last month of the fiscal year. Because of the way funds are allotted to specific properties, some will fall short on several months of funding.

For the sake of our constituents, this trend has to stop.

The federal government has always been on the forefront of investments in rural America. From the Tennessee Valley Authority bringing electricity to lower Appalachia to the construction of a sophisticated network of levees that has kept flood waters out of the Mississippi Delta, the federal government has always been there making forward-thinking investments that foster economic stability and advancement. Now is not the time to reverse course and simply leave opportunity for progress in our country to the profit-driven private sector.

Rural America possesses an abundance of untapped potential. Sure, the challenge is great but our dreams can be realized with wise investment by the federal government. It is time to recommit ourselves to building a nation for all Americans. I am ready to continue the good fight, and I know that you are, too. Hopefully, more of my colleagues will join us in improving housing conditions in rural America.

Mr. Thompson, formerly Mayor, Town of Bolton, MS and Supervisor, District Two, Hinds County, Bolton, MS, is currently the U.S. Representative of the 2nd Congressional District of Mississippi. He is the top Democratic member of the House Committee on Homeland Security. A lifelong activist in the civil rights struggle, Rep. Thompson has received honors from the National Conference of Black Mayors, USDA Rural Development Fellows, Mississippi Chapter of the NAACP, and the Ford Foundation. Directorships include the American Civil Liberties Union, the Housing Assistance Council, the Southern Regional Council, and the National Rainbow Coalition.

by Leslie Newman

This story appears in the 2015 Fall Edition of Rural Voices

“Self-help is not a new concept for us. We were always self-help, traditionally. We always built our own homes. We didn’t wait. We have to get away from this dependence and go back to protecting our own assets. A long time ago, if a teepee tore, they didn’t wait for someone else to come sew it up. We had to have that shelter.” –Pinky Clifford, Executive Director, Oglala Sioux Tribe Partnership for Housing

by Leslie Newman

This story appears in the 2015 Fall Edition of Rural Voices

“Self-help is not a new concept for us. We were always self-help, traditionally. We always built our own homes. We didn’t wait. We have to get away from this dependence and go back to protecting our own assets. A long time ago, if a teepee tore, they didn’t wait for someone else to come sew it up. We had to have that shelter.” –Pinky Clifford, Executive Director, Oglala Sioux Tribe Partnership for Housing.

In fall 2003, we looked at a new self-help housing program on the Pine Ridge Indian Reservation, developed by the Oglala Sioux Tribe Partnership for Housing (OSTPH). We looked at what it took to create the program, some challenges to self-help housing on tribal trust land, and ingredients for success.

In fall 2003, we looked at a new self-help housing program on the Pine Ridge Indian Reservation, developed by the Oglala Sioux Tribe Partnership for Housing (OSTPH). We looked at what it took to create the program, some challenges to self-help housing on tribal trust land, and ingredients for success.

Now, going back to Pine Ridge more than ten years later, we find that self-help is alive and well. While the OSTPH is no longer operating a USDA Rural Development self-help program, it is still committed to the self-help concept, and another organization, Thunder Valley Community Development Corporation, has recently been awarded Section 523 funding from Rural Development to develop and launch a self-help pilot. Through a unique collaborative effort, the Sustainable Home Ownership Program (SHOP) collaborative, the two organizations and other partners are working together to promote homeownership on Pine Ridge and support each other’s efforts.

The Oglala Sioux Tribe Partnership for Housing is a private, nonprofit organization promoting homeownership and developing viable housing options for people on the Pine Ridge Indian Reservation. Over the past 16 years, OSTPH has worked to promote homeownership there, providing homeownership education and counseling, assisting families in applying for home mortgages, and building homes to meet the severe housing shortage on the reservation. The organization has assisted over 90 families in purchasing homes. Through its self-help program, a total of 24 families worked together to build their own homes. These homes are scattered in different districts around the reservation, an area spanning approximately 40,000 square miles (the size of the state of Connecticut).

After these 24 families constructed their homes, the organization determined that it would pursue self-help housing in other ways. According to executive director Pinky Clifford, “Self-help with Rural Development is one thing, but there are other options to look at.” OSTPH is currently working with partners to design and develop a “tiny house” program, enabling families to work together to build a home that could be moved easily on a flatbed truck to a location of their choice (it would not require special house-moving equipment). Learning from their experience working simultaneously with multiple families across the reservation, the OSTPH envisions that with its new self-help programming, participating families will completely build one home, and then start building the next. “We’re looking at self-help, one family at a time,” explains Clifford. The OSTPH sees the “tiny house” program as a key to long-term asset-building, as families can build onto the small house over time, or sell a house to another family and use the equity as a down payment to buy another home.

In order to address the need for improvements to existing homes, the OSTPH is also looking at a self-help rehab program. According to Clifford, “there are hundreds and hundreds of homes that need to be rehabbed. We’re looking for innovative ways to access resources to make this happen.”

Thunder Valley Community Development Corporation is an Oglala-led, Native American 501(c)(3) nonprofit organization based out of the Thunder Valley community of the Porcupine District on the Pine Ridge Indian Reservation. Its mission is “empowering Lakota youth and families to improve the health, culture, and environment of our communities, through the healing and strengthening of cultural identity.” Thunder Valley is currently implementing a comprehensive community development initiative, which includes the creation of homeownership opportunities, a youth shelter, an empowerment center, community gardens, a walking/hiking/biking trail, a business incubator, commercial space, a bunkhouse for volunteers and students, and powwow grounds.

Thunder Valley sees the self-help approach as an important piece of its comprehensive efforts to build a community, and emphasizes that its program builds on the work and experience of the OSTPH. According to executive director Nick Tilsen, “We don’t believe that Thunder Valley would be afforded the opportunity to take on self-help on Pine Ridge if Pinky and the [Oglala Sioux Tribe] Partnership hadn’t done it before and paved the way. They showed that self-help can be done. We wanted to take it on because it works.”

In developing its self-help pilot program, one of Thunder Valley’s first steps focused on learning about the OSTPH efforts. Liz Welch, Thunder Valley’s director of advancement, explains that “the Partnership was transparent and open to share their experience, both what worked and what was really challenging. Without that, we wouldn’t have taken it on.”

Rather than scattered sites, Thunder Valley self-help participants will be building homes in the Thunder Valley development in Porcupine. According to Tilsen, community and relationship building is a major reason that Thunder Valley believes in the self-help model: “Because we’re building an actual physical community – beyond building homes, we’re trying to build relationships between the families. By helping one another build their houses, we’re building positive, healthy relationships between neighbors.”

Architectural rendering of Thunder Valley’s Regenerative Community Development Plan, courtesy of Thunder Valley CDC

Architectural rendering of Thunder Valley’s Regenerative Community Development Plan, courtesy of Thunder Valley CDC

Like many self-help programs around the country, Thunder Valley recognizes that sweat equity is key to making homeownership affordable for low-income families and to long-term asset building. Affordability also underlies the organization’s commitment to green building and energy-efficient construction. “We’re on a pathway,” Tilsen explains. “Our end goal is to build affordable housing with net-zero energy costs. We strongly believe that low-income families shouldn’t be dumping their limited resources into utility bills and high energy costs. Instead, we want them to put their resources into building assets.” Thunder Valley’s energy efficient construction includes using passive solar design (orientation of homes, placement and size of overhangs), as well as solar panels and solar thermal systems.

Thunder Valley is currently focusing on infrastructure development for its new community (roads, water, sewer) and preparing its first group of six self-help families. Through its pilot program, a total of 12 families will build their new homes in the development; the first six are scheduled to begin construction in the spring/summer of 2016.

In looking at self-help housing in Pine Ridge back in 2003, it was clear that collaboration was key to the success of homeownership efforts. In speaking with the OSTPH and Thunder Valley today, this spirit of partnership is still apparent, if not stronger. Through the SHOP collaborative, Thunder Valley and the OSTPH are working with other partners to streamline the homeownership process on Pine Ridge and support one another’s efforts. Through the collaborative, partners have developed a shared training calendar, make IDA program homeownership referrals, and share other homeownership opportunities. Tilsen explains, “We are working to support and promote each other’s efforts. Even if a potential homebuyer isn’t a good fit for our program, we can refer them to one of our partners. The only way we know about other opportunities and what our partners can offer is by collaborating and working together.”

Back in 2003, we saw that developing self-help housing on Pine Ridge was not an easy task, and this has not changed. The joint efforts and partnerships we see today are a critical part of successful self-help housing efforts and providing homeownership opportunities for tribal members, and a model for other communities around the country.

Leslie Newman is a founder and co-manager of Seven Sisters Community Development Group, which focuses on community development in Native communities. She has been working to support affordable housing and asset building on the Pine Ridge Reservation since 1999.

by Kim Herman

This story appears in the 2015 Fall Edition of Rural Voices

Tax credits remain important in rural Washington, financing the production of thousands of homes.

by Kim Herman

This story appears in the 2015 Fall Edition of Rural Voices

Tax credits remain important in rural Washington, financing the production of thousands of homes.

That statement was in the opening paragraph of a 2003 article for Rural Voices I wrote about the use of housing tax credits in rural Washington. Without a doubt, it is just as true today as it was then, if not more so. In the intervening 12 years, the Washington State Housing Finance Commission has amended our housing credit guidelines a number of times, we participated in the tax credit support programs created by federal economic recovery legislation in 2008 and 2009, we survived the Great Recession, and we have redefined the geography of Washington for applicants for the 9 percent tax credit program. What has not changed is the importance to rural Washington of the housing credit program, which encourages private sector investment in affordable rental housing properties.

In my 2003 article I was able to point to 121 rural housing projects funded with housing credits that produced more than 4,000 units of affordable housing. I am happy to say that since that time our production of affordable rural housing using housing tax credits has not slowed down. Since 2003, we have financed another 191 rural projects providing another 8,844 affordable housing units in rural communities with populations of less than 50,000. Even more interesting is that 44 of the projects were financed using tax-exempt bonds and 4 percent housing credits, removing pressure from the resource-limited 9 percent credit program.

In many smaller communities where projects have previously been built, there have been fewer opportunities for feasible rural developments. We have also experienced less for-profit involvement in rural areas due to the scoring criteria in the competitive 9 percent program. Now, however, we see smarter and more sophisticated nonprofit developers expanding their reach.

These changes were driven by the competition and economics of the tax credit program and the need for trust and confidence to be developed between the developers of rural housing and tax credit investors. Small rural projects became less feasible as land and building costs increased and the program came under scrutiny about high per-unit costs. Therefore, we have seen the number of units in rural projects increase.

In addition, both for-profit and nonprofit developers have taken advantage of opportunities for acquisition and rehabilitation of older USDA Section 515 portfolios, often using the bond/4 percent credit program instead of the 9 percent program. Even more could be done to preserve USDA’s aging rural housing portfolio if the agency would streamline its processing time and remove outdated requirements that force tax credit allocators to repeatedly roll over allocations for the purchase and preservation of USDA projects already in the pipeline.

The Commission had financed two housing credit projects for Native American tribes in the early 2000s in cooperation with Travois, a national organization serving tribal housing authorities. Then we reached out to the tribes and provided specific training in the housing credit program to encourage more tribal participation. This effort increased successful applications from tribes in Washington. Since 2003, we have financed an additional 11 projects for various tribes that provide 321 affordable housing units to tribal members. Given the remote location of many tribal reservations, including the Makah tribe in the far northwest corner of Washington, these financings demonstrate the wonderful flexibility of the housing credit program in rural America.

In the first year of the Great Recession, 2008, the Commission took advantage of a 20 percent increase in Washington’s per-capita credit allocation and an expanded definition of projects eligible for the 30 percent basis boost to finance seven housing credit projects in rural Washington that provided 375 units of affordable housing to low-income households. These benefits were part of the Housing and Economic Recovery Act (HERA) passed the same year to stimulate the economy.

The federal efforts to support the housing credit program under the 2009 American Recovery and Reinvestment Act (ARRA) provided even greater stimuli for helping rural projects in Washington. While not all of the benefits went to rural projects, ARRA combined $37.8 million in the Tax Credit Assistance Program and $101 million generated through the Section 1602 Exchange Program with $96.8 million in regular 2009 housing credits to fund almost twice as many projects as usual. This included 12 rural projects with 480 units of housing for low-income families and represented a significant economic boost to rural communities that were suffering the effects of the recession.

In 2013, the Commission made a number of significant changes to our allocation criteria for the 9 percent housing credit program. These changes allowed us to improve the balance of the allocations across the state geographically, as well as to address the growing conflict between the need to preserve existing housing and the priority to create new units. After much research and many stakeholder policy meetings, we eliminated our credit set-asides for Rural Development (RD) projects, qualified nonprofits, and rural areas, as well as the “Housing Needs Points” previously used to determine geographic distribution.

Instead, three distinct geographic credit pools were created: King County Metro (home of Seattle), other metro counties, and nonmetro counties. Like projects now compete against like projects, based upon the pool in which they are located. This also provided the opportunity to evaluate and adjust the existing allocation criteria and their applicability to the various geographies, which removed several barriers for rural projects to compete for housing credits. The Commission also introduced significant total development cost guidelines the same year that were adjusted to match economic factors in the three geographic pools. These changes resulted in seven rural projects receiving housing credits in 2013, producing 432 units of affordable rural housing.

The Low Income Housing Tax Credit program has allocated $853.8 million in housing credits to fund 312 rural housing projects that have produced 8,165 units of family housing, 3,534 units of senior housing and 1,145 units of housing for agricultural workers in Washington State. Beyond a doubt, without the housing credit program, the vast majority of the people living in these affordable homes would not have a decent, affordable place to live today.

Kim Herman is Executive Director of the Washington State Housing Finance Commission. His past experience includes executive positions at Delta Housing Development Corporation, Indianola, MS; Rural Housing Alliance/Rural America, Washington, DC; Rural Assistance Initiative, HUD; Yakima Housing Authority, Yakima, WA; and Portland Development Commission, Portland, OR.

by Mary Brooks

This story appears in the 2015 Fall Edition of Rural Voices

Over the last 30 years of experience with housing trust funds, an amazing movement has been sustained and brightened by the tenacity and creativity of affordable housing/homeless advocates across this country. One could take a close look at almost any aspect of critical affordable housing needs in this country and see it being addressed within the housing trust fund community. The success of the housing trust fund movement offers undeniable evidence that we can provide everyone in this country with a safe affordable home. While the needs yet to be addressed are strikingly huge, if we committed the resources needed, we could end homelessness and provide safe affordable homes for all. It is an issue of resources and a challenge to the political will of this country.

by Mary Brooks

This story appears in the 2015 Fall Edition of Rural Voices

Over the last 30 years of experience with housing trust funds, an amazing movement has been sustained and brightened by the tenacity and creativity of affordable housing/homeless advocates across this country. One could take a close look at almost any aspect of critical affordable housing needs in this country and see it being addressed within the housing trust fund community. The success of the housing trust fund movement offers undeniable evidence that we can provide everyone in this country with a safe affordable home. While the needs yet to be addressed are strikingly huge, if we committed the resources needed, we could end homelessness and provide safe affordable homes for all. It is an issue of resources and a challenge to the political will of this country.

More than 750 housing trust funds in cities, counties, and states throughout the United States are providing hundreds of millions of dollars to support needed safe affordable homes. Housing trust funds receive dedicated sources of public funds to provide an ongoing source of financing to support affordable housing for those most in need. A housing trust fund is typically established through a local ordinance or state law that creates the fund itself, identifies an administrative structure for overseeing its operation, establishes regulatory requirements for expenditure of the funds, and enables the dedication of identified sources of public funds.

Forty-seven states have created housing trust funds, although three of these have yet to commit revenue to the funds. While all state housing trust funds distribute funds across the state, at least Illinois, Kentucky, Nebraska, Nevada, Ohio, Oklahoma, Texas, Utah, and Washington either set aside a portion of available funds to be used specifically in rural areas of the state or are subject to a statutory target to do so.

Despite having dedicated public revenues, housing trust funds suffered greatly during the last recession. Committed revenue streams collected reduced amounts of money and, in several states, funds were used to patch budget deficits. Now all indications are that this is reversing, with several states renewing, if not building, their support for state housing trust funds. Just in the last year wins occurred in Connecticut, Florida, Hawaii, Minnesota, North Dakota, Ohio, Vermont, Virginia, Washington, and Washington, D.C. And several advances, including new housing trust funds, have been created at the local level.

State housing trust funds have learned how to brag about the affordable homes they have made possible throughout their states, including rural areas. There are lots of good reasons for this. First, it informs elected officials about the value of investing in affordable housing within the entire state, including the areas they represent. Second, it illustrates the importance of state funds supporting affordable housing and the flexibility these trust funds can provide, recognizing that affordable housing in different parts of the state may require different approaches. Third, it demonstrates what is possible – what can be accomplished if we commit the resources to make it work.

The single most commonly expressed advantage of creating local and state housing trust funds is the flexibility they provide in addressing a wide range of housing/homeless needs. Housing trust funds are designed to meet specific objectives, most often including serving those with the lowest incomes, ensuring long-term affordability, meeting accessibility and energy efficiency standards, and providing support throughout the state to all geographic areas. Yet, at the same time, they can also be called upon to meet unique challenges and take advantage of immediate opportunities.

The South Dakota Housing Opportunity Fund established a special application process to address the devastating impact of the Delmont tornado – a good example of how these flexible funds can be drawn to address unique, and in this instance urgent, circumstances. The simple application allows funds to be used for down payment assistance, home reconstruction, rental or utility deposits, or purchasing appliances.

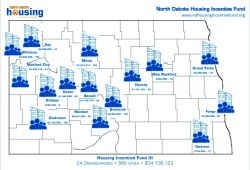

The illustrations here show how North Dakota and Ohio have made funds available across the state in a wide variety of geographic areas.

|

|

|

| NORTH DAKOTA’S HOUSING INVESTMENT FUND | |

|

North Dakota’s Housing investment Fund is sustained through contributions in exchange for tax credits and funds from the Bank of North Dakota. The Fund has supported more than 2,000 affordable homes and averaged an additional $4 for every $1 invested by the fund. |

|

|

|

| THE OHIO HOUSING TRUST FUND | |

|

The Ohio Housing Trust Fund is supported through revenues collected form document recording fees. Currently, the fund distributes grants and loans through these five programs:

|

|

|

|

The Nebraska Housing Developers Association provides some insight into how the nonprofit and for-profit development communities have been integral to the success of the housing trust fund movement. “Nebraska uses its Housing Trust Fund to support development of rental housing in rural Nebraska,” explains Danielle Hill, Executive Director of the Association.

“The availability of rental housing in rural Nebraska is critical to the economic viability of many small communities. Other housing resources, such as the Low Income Housing Tax Credit, are not as efficient when fewer than 12 units are being developed. In many of Nebraska’s rural communities, contractor jobs and material supply companies are supported through the development and or rehabilitation of housing. This same development adds to the community’s tax base.”

The Nebraska Affordable Housing Trust Fund is statutorily required to allocate at least 30 percent of annual revenues to each of the state’s three congressional districts. Within its first ten years of operation, the Fund awarded nearly $88 million, which was matched with more than $300 million in other public and private funds. This helped support 4,765 affordable homes throughout the state and created at least 6,300 jobs.

The availability of rental housing in rural Nebraska is critical to the economic viability of many small communities.

Another promising advance in the housing trust fund field has occurred in states that have passed enabling legislation either encouraging the creation of local housing trust funds and/or making revenue options available to them. These state enabling programs vary across the country but the evidence indicates real impact across the states. Here are just a few examples.

Pennsylvania: Act 137 enabled counties to increase their document recording fees if the funds were committed to affordable housing activities. More than half the counties in the state have done so and funds are used to support a variety of activities from senior citizen housing to owner-occupied rehabilitation work to financial assistance for developing rental housing.

Florida: A majority of the funds in the Florida state housing trust fund support the State Housing Initiatives Partnership Program, allocating funds, based on a formula, to every county within the state and to entitlement cities.

Washington: The state passed legislation that increased the document recording fee and allocates these funds to each county to address homelessness.

Massachusetts: The Community Preservation Act has enabled more than 150 communities to enact a surcharge on real property taxes to create local dedicated funds for four purposes: affordable housing, open space preservation, historic preservation, and outdoor recreation. Creation of these funds also triggers annual distributions from the statewide Community Preservation Act Trust Fund, which derives its revenues from fees collected at the state registries of deeds.

Iowa: The Iowa Housing Trust Fund reserves at least 60 percent of its revenue for the local housing trust fund program, matching what local funds can generate throughout the state. At this point, 27 city, county, and regional local funds have been certified as eligible to receive matching state funds.

The housing trust fund movement’s strong history has enabled affordable housing/homeless advocates across the country to integrate new elements into statewide and local campaigns that are proving to be particularly effective.

First, many economic benefits of investment in affordable housing can be documented. The money housing trust funds commit to affordable housing activities leverages additional funds from other public and private sources, bringing additional revenues into communities. Studies across the country highlight the full range of economic benefits, including job creation, tax revenues, and more. Here are a few examples.

The second is the power of putting a face to the value of home. Numerous studies (many supported through the MacArthur Foundation’s How Housing Matters to Families and Communities initiative) have documented housing’s effects and the relationship between safe affordable homes and school performance, health benefits, environmental quality, and so much more. The stories individuals and families can share about how their lives are impacted when they secure affordable homes brings a powerful perspective to why these initiatives do matter. The Housing Assistance Council has recognized this for many years in sharing many of these stories in Rural Voices. Many campaigns and the affordable housing/homeless coalitions that wage them have incorporated videos, postcards, and stories to bring their messages home.

Recognizing the breadth of safe, affordable housing’s impact on communities has also brought into perspective just how housing does matter in terms of many related issues, including education, health, environment, employment, and much more. This has enabled many affordable housing/homeless coalitions to build cross-issue alliances integrating new and inspiring perspectives into the challenge of securing additional resources to meet the need for affordable housing.

Finally, a very exciting element of movement building is being considered in several states focused on the engagement of residents in affordable housing complexes, empowering them to bring their voices to affordable housing/homeless advocacy. These efforts could enable thousands to join these campaigns. From gathering postcards, to Twitter storms, to engaging in lobby days, hearing from those who have benefitted from the very affordable housing/homeless policy changes accomplished throughout the country is a striking statement of success and the promise of what we can do … when the will is there.

Mary Brooks works at the Housing Trust Fund Project of the Center for Community Change, housingtrustfundproject.org.

This story appears in the 2015 Summer Edition of Rural Voices

This story appears in the 2015 Summer Edition of Rural Voices

by Tom Vilsak, Secretary of Agriculture

As Secretary of Agriculture I’ve had the opportunity to visit hundreds of small towns all across America. I’ve seen firsthand the strength and resilience of rural business and families, and the positive impact of USDA employees and programs to help rural communities thrive.

Still, too many of our fellow citizens are being left behind. Too many of our small towns are struggling. Although they are some of the hardest working folks I know, rural Americans earn, on average, $11,000 less than their urban counterparts each year. They are more likely to live in poverty.

I have a specific memory of rural poverty from a long time ago that has left an indelible mark on me. My son and I volunteered to help build homes for migrant farmworkers in McAllen, Texas. That experience exposed us to the tough lives these families live.

Despite their circumstances, they are extraordinary, hardworking and humble people. They deserve to live in safe houses. They deserve the opportunity to turn those houses into homes for their families. I know the Housing Assistance Council and other housing advocates feel the same way.

That experience made me proud to serve at a Department that provides programs and services that help rural families climb out of poverty and move into the middle class. For example, our nutrition programs help hardworking moms and dads as they search for good paying jobs that will allow them to put healthy food on the table for their kids without assistance.

Another example is our self-help housing program, which for the past fifty years has helped low- and very low-income families build their own homes. For many of these families, their self-help house is the first time in their lives they’ve lived in a real house.

Hard work and dedication reduces construction costs and, paired with an affordable USDA mortgage, makes homeownership possible for families that would not otherwise be able. Working with local support organizations, families spend long hours in the evenings and on weekends working on their homes. The families frame the houses, install roofs, put up windows and siding, and paint. Each of the 870 families that participated in the program last year built about $27,500 in sweat equity in their brand-new homes.

This program also helps increase homeownership among women and minorities living in rural communities. Over half of agency-financed self-help homes are built by minorities. Since 2008, 41 percent of self-help homes have been built and bought by women-led households, many of whom are single mothers.

For example, in the span of just three years, Christy Milburn and her two young children lived in fifty-five different places. A couple weeks on a couch here, stay in a spare room there, and by 2006 she had run out of friends and couches. As a homeless single mother in Montana, Christy came to Missoula to once again try to get her life back on track. A string of bad luck and regrettable personal decisions had put her in a position she didn’t want to face, yet didn’t know how to escape.

“I would take my kids out for a walk, just for something to do,” said Christy. “We’d be walking down a street and I’d see a family inside their home – behind that picture window – and I’d wonder if I could ever get my life straightened out, and find that stability to just live in the same place for more than a few weeks.”

USDA and partners in Montana, including the Missoula Housing Authority and NeighborWorks Montana, teamed up to help Christy and her kids build and move into one of ten affordable homes in a subdivision just west of Missoula. Today, Christy is able to provide the stability for her children that she had dreamed about for so long.

Recently, the first successful self-help project in Indian Country has provided homeownership to three women-headed families, the first of twelve planned homes in the Zuni Pueblo of New Mexico. These families have never owned a home and many have been renting for 15 years or more. Kay, one of the participants in the program, described her motivation for putting in the long hours and hard work needed: “I live for my kids, so, what I do is practically just for them.”

Stories like Kay’s and Christy’s make me proud of the work that USDA does in rural communities. I am proud to say that we will soon celebrate a new milestone-our 50,000th self-help home-this summer. Together with dedicated partners like the Housing Assistance Council, we are helping rural families achieve the American dream of homeownership. Thank you for your partnership and keep up the good work.

Tom Vilsack serves as the Nation’s 30th Secretary of Agriculture. As leader of the U.S. Department of Agriculture (USDA), Vilsack is working hard to strengthen the American agricultural economy, build vibrant rural communities and create new markets for the tremendous innovation of rural America. In six years at the Department, Vilsack has worked to implement President Obama’s agenda to put Americans back to work and create an economy built to last. USDA has supported America’s farmers, ranchers and growers who are driving the rural economy forward, providing food assistance to millions of Americans, carrying out record conservation efforts, making record investments in our rural communities and helped provide a safe, sufficient and nutritious food supply for the American people.

This story appears in the 2015 Summer Edition of Rural Voices

by U.S. Representative Harold “Hal” Rogers

In May 2015, Governor Steve Beshear (KY-D) and I joined over a thousand residents of southern and eastern Kentucky at the second SOAR (Shaping Our Appalachian Region) Summit. Our shared goal in this truly grassroots initiative is to expand job creation, enhance regional opportunity, innovation and identity, improve the quality of life, and support all those working to achieve these goals in Appalachian Kentucky. Ensuring that everyone in our rural communities has access to quality, affordable housing options is a critical component of our strategy to advance a thriving, vibrant region.

For years, I have had the pleasure of witnessing local organizations like the Federation of Appalachian Housing Enterprises and Kentucky Habitat for Humanity foster critical federal partnerships in order to make a meaningful impact at the community level. Unquestionably, the relationship forged with the U.S. Department of Agriculture (USDA) Rural Development in southern and eastern Kentucky, and communities around the country, plays an important role in improving the economy and the quality of life in these rural areas.

As Chairman of the House Appropriations Committee, I have the responsibility of overseeing the allocation of federal spending, and during a recent budget hearing with the USDA for fiscal year 2016, I had the opportunity to highlight a number of important USDA Rural Development programs that impact rural citizens nationwide. For example, I applauded the agency’s support for the single-family direct loan program. This program helps the poorest in rural America achieve the dream of owning a home, and for this reason, it continues to be one of USDA Rural Development’s most successful initiatives.

Another successful federal-local partnership which has been impactful in my region is the USDA Rural Development Section 504 Home Repair program, which is designed to help very low-income rural homeowners repair, improve, or modernize their homes and remove potential health and safety hazards through low-interest loans or grants. Many elderly homeowners in my district take advantage of the Section 504 Home Repair program, which allows them to safely stay in their own

homes longer.

The USDA Rural Development Mutual Self-Help Housing program has also proved life-changing in my rural Eastern Kentucky district, and other rural districts across the country. Those collaborating on Mutual Self-Help have made homeownership an option for countless low-income families that are willing to contribute sweat equity. The value of this housing program to families is best illustrated through the smiles on a family’s face when they are moving in to the home that they helped complete.

For example, a single mother in my district recently shared her inspiring story of success with the Self-Help program. She initially signed up because she wanted a safer environment to raise her son. Determined to improve the future for herself and her son, she tirelessly worked nights and weekends to build her own home. Not only did she improve the living situation for her small family, she also says her son’s attitude and grades have even improved. Simply put, without the Self-Help Housing Program that allowed her to contribute to the process, she would not have been able to afford her new home.

This year, the 50,000th family will have utilized the program to complete their homes, and I hope many more in the future will have the opportunity to turn their lives around in the same manner.

Serving Kentucky’s 5th Congressional District since 1981, Hal Rogers is currently in his 18th term representing the people of southern and eastern Kentucky, and is the longest serving Kentucky Republican ever elected to federal office. Focused on economic development, job creation, fighting illegal drug use and preserving the natural treasures of Appalachia, Rogers has a reputation for listening to his constituents and fighting for the interests of the region where he was raised. Nationally, as Chairman of the powerful House Appropriations Committee, his focus is on reducing the size and scope of the government by reining in federal spending, conducting rigorous but thoughtful oversight of federal agencies, and restoring fiscal discipline and transparency to our budget process.

This story appears in the 2015 Summer Edition of Rural Voices

by U.S. Representative Sam Farr

The American dream is built on homeownership. For generations, American families have benefited from investing in their first home. It gives them a sense of community, it is a source of pride and for most homeowners it is their most valuable asset.

Unfortunately, the door to homeownership is too often closed for many individuals. That is why the U.S. Department of Agriculture’s Self-Help Housing program is so valuable. For 50 years, self-help housing has given low-income Americans in rural areas the chance to own their first home – not through a hand-out but instead through a hand-up.

I was a Peace Corps volunteer in Colombia where I saw the culture of poverty first hand. I watched it hold down entire barrios; preventing whole communities from building a better life for themselves. Breaking that cycle of poverty requires access to things like health care, food and an education. But before any of those needs can be met, you first need a safe place to sleep at night, not just a roof over your head but a home that serves as foundation for everything else.

That same cycle of poverty still exists in rural America. It prevents our communities from reaching their full potential. If we want to break that cycle of poverty, we need to invest in building more affordable housing. That means lowering the cost to construct new homes and lowering the income threshold for home financing.

Self-help housing achieves both of those goals. On average, self-help homes cost $120,000 less than a typical new home to build. And participants gain financing despite earning $20,000 less than the U.S. median income. Self-help housing achieves these dual goals by literally giving people the tools necessary to build and own their first home.

Participants in self-help housing aren’t just handed the keys to a new home. They help build it from the ground up. About 65 percent of the labor is provided by homeowners, allowing folks to start out with equity in their home – sweat equity. Imagine the pride a homeowner feels when they first cross the threshold into their new home. Now imagine how overwhelming that pride must be if they knew, not only did they build that home but they now have the skills to maintain it for life.

That new found knowledge is why self-help housing participants are more likely to remain in their home. In fact, some of the first families to benefit from the program still live in their original homes 50 years later. What they started in Goshen, California five decades ago has now helped families all across rural America realize their own slice of the American dream.

That historical connection to California is one of the many reasons I support this wonderful program. In my district on the Central Coast of California, organizations like South County Housing and Community Housing Improvement Systems and Planning Association, Inc. (CHISPA) work with new homeowners to finance and build their first home through this program. They fill a niche in our rural counties that desperately need access to more affordable housing.

Self-help housing is doing more than just building homes…it is building whole communities. Participants do not just build their home on their own. They work side-by-side with their neighbors. Families work together to build safe, affordable housing for each other to enjoy.

And isn’t that what rural America is all about? Neighbors helping their neighbors build a better life for each other. That is the foundation of a community. That is the real American dream. A dream that USDA’s Self-Help Housing Program has helped come true for 50 years.

Congressman Sam Farr has represented California’s Central Coast for 23 years. His district, known as the Salad Bowl of the World, encompasses the Monterey Bay region and the Salinas Valley. He currently serves on the House Committee on Appropriations and is the Ranking Member on the Subcommittee on Agriculture Appropriations. Prior to serving in Congress, Farr served twelve years in the California State Assembly and six years as Monterey County Supervisor. He began his career in public service in 1964 serving in the Peace Corps in Colombia.