The Power of Working Together

Three families share their experiences with USDA’s Mutual Self-Help Housing Program

This story appears in the Fall 2014 issue of Rural Voices

This story appears in the Fall 2014 issue of Rural Voices

Mutual Self-Help is a USDA Rural Development program administered by community-based nonprofit housing organizations that makes housing affordable through “sweat equity”. Families work together as a group to build approximately 65 percent of their homes. This labor not only acts as the down payment, but can substantially reduce the price of the home. However, it is hard work and it does require commitment. Households work together, with each family contributing a minimum of 35 hours of labor per week for approximately 8 to 12 months. The homes are built simultaneously; no one moves in until all the homes are completed.

Dillan and Lacie; Rebecca; and Anita and Robbie all participated in the Neighborhood Nonprofit Housing Corporation (NNHC) mutual self-help program. Below each family recounts their challenges, successes, and experiences building their own home and helping other families build theirs.

How did you first hear about self-help housing?

Dillan: When attending school, Lacie and I had no thoughts of buying, let alone, building a brand new house. Because I am a student, the idea of securing a home loan was near impossible, until we heard about Neighborhood Nonprofit’s housing program. A family member mentioned to me an advertisement they had seen in the newspaper one day and I just stopped in the office to see what it was about. Ten months later here we are in the final stages of building our beautiful new home. The process was very simple to qualify for the program and the Neighborhood Nonprofit staff was very helpful.

Dillan and Lacie are both originally from Cache Valley, UT and wanted to raise their children there. Lacie is a stay at home mom. Dillan is a returning student at Utah State University and plans to be a teacher.

Dillan and Lacie are both originally from Cache Valley, UT and wanted to raise their children there. Lacie is a stay at home mom. Dillan is a returning student at Utah State University and plans to be a teacher.

Rebecca: I had previously heard about Self-Help housing a couple of years before applying, but I did not want to make such a major decision so soon after my husband’s death. I also didn’t see how I would be able to put in the time needed to build as a single mother. It wasn’t until after I tried unsuccessfully to find affordable housing for my family that I decided to throw in my application and see what happened.

Anita: We heard about the Self-Help program from one of my husband’s coworkers. They had built in the nearby town of Nibley, UT. We decided to look into the program after looking for houses to buy became discouraging. We knew that my staying at home with our children would make it difficult to afford one. We were also excited about the opportunity to learn the skills involved with building a house. We are grateful we learned these skills because we feel more prepared to maintain our home.

What was the construction process like?

Anita: During the time we built, life was so busy! I was pregnant when we started, so my husband did most of the work for the first several months. Life was hard but we were excited for the end result. It took our group ten months to finish all our homes. We worked with really great people. Everyone had the same attitude to work on each other’s home like it was their own. This created a positive working environment. I would say the hardest challenge we faced was everyone getting burned out and not working as fast as we had hoped. I was glad to be able to go out and work too. Working together on our home taught us a lot and was a great benefit to us recently when we finished our basement.

Dillan: While the qualification process was simple, the building process has not been quite as simple. Building each home together has been challenging and rewarding at the same time. The families in our group have worked so hard together and have accomplished so much. The program has not been easy, but it has been worth it. I believe that each family will leave the program with a greater sense of community and friendship because of the hard work that everyone has endured.

Rebecca: My youngest was only three when I started building! Since my oldest was just 12, I was the only one in our family that was able to work on the homes. To be honest, it was a difficult process for me to build; besides having five children and no spouse, I am a student at Utah State University. A typical day would start at 4:30 a.m. I had to get up that early to get everything ready for the day, including dropping off my children at school and getting myself to class. After school was out, I would have to rush to pick up my children and take them to a baby sitter (none of them were old enough to be on the site) and then get myself to the work site. I usually wouldn’t get home until after 10:00pm. I still had to put kids to bed, take a shower (get all the sawdust and grime off that I’m allergic to), and do regular household chores.

Rebecca is a widow with five children ages 16, 15, 12, 10, and 7, and is currently a student at Utah State University pursuing a degree in Social Work.

Rebecca is a widow with five children ages 16, 15, 12, 10, and 7, and is currently a student at Utah State University pursuing a degree in Social Work.

What were your living conditions before and after your participation in the self-help program?

Rebecca: Before [the Self-Help program] we had been living in a three-bedroom apartment for about two years. It was definitely cramped; my two daughters shared one bedroom, and my three sons shared another bedroom. We all needed some personal space. In addition, the apartment would flood occasionally, so it had mold and mildew issues and smelled terrible. It was also where we were living when I lost my husband and the children lost their dad. That apartment created some difficult memories for us. It was really healthy, both physically and emotionally, for us to get out of that environment. Every day, I count my blessings – I have a house, a yard, and good neighbors. I love the neighborhood! One especially nice benefit to having our home is having a back-yard big enough to grow a garden. I could never afford to buy fresh produce for my family. Now, we eat fresh food that we’ve grown ourselves!

Anita: Before we built our house, we lived in a townhouse. The community was nice but the main thing that was missing was a private backyard. One of my favorite features of the program was being able to move in having our landscape and fences included in the building process. I love being able to send my own kids out to have fun in our large fenced-in area. One other major unexpected benefit to having a fenced-in backyard was that it helped my preschool business. My city requires all new preschools to have a fenced-in backyard. This could have been an expensive hurdle but thanks to the Self-Help specifications, this was included.

Anita and her husband Robbie have three children all under the age of six. Anita is a stay at home mom who started her own preschool business. Robbie is a conference coordinator for Utah State University.

Anita and her husband Robbie have three children all under the age of six. Anita is a stay at home mom who started her own preschool business. Robbie is a conference coordinator for Utah State University.

Dillan: Before the Self-Help program and as students with a large family, our housing conditions have been, at times, hard to deal with. Now that we are able to have a home to call our own it has given our family and especially our children a place to feel comfortable and more importantly a place to stay for a long time. We now have a “Room with a View,” a place to grow together and create lasting memories.

What specific successes or challenges did you experience?

Dillan: A challenge we faced in our group was learning to work together on a home that wasn’t your own. The workmanship as well as the attitude of all the families involved improved once everyone truly figured out that no one could move in to their own homes before the other houses were completed. No work was completed without the thought of “If it was my home, would I do it like that?” When this concept was grasped, the work excelled in speed and accuracy. Although this and other things were challenges, the successes far exceeded them. A friendship has been made between the families as we worked hard together.

Rebecca: It took a lot of determination to get my weekly hours in and keep up with my other responsibilities. Because it is easier to meet the time requirements if the family is a two parent household (it’s estimated that both husband and wife can come in together one day a week), I had to go in outside of the group’s regular work hours in order to work my full 35 hours per week. During the building process, I had to have two surgeries on my broken leg. While on crutches, and not allowed on site, I had good people that helped donate hours so I could keep up.

I love the neighborhood. I got to know my neighbors really well while we built – both the good and the bad! We learned to work with everyone’s personalities, and I think we learned the importance of not saying things we would regret later. Now, we have a real sense of taking care of each other. It is like having a built-in Neighborhood Watch Program! I have developed some very good friendships from the time we spent building together.

Anita: We are very grateful to have been able to build our home through the Mutual Self Help process. We learned a lot from our construction supervisor and have a lot of respect for him. He made sure things were done the right way. The process was hard; but worth it because we not only got a beautiful home but gained knowledge and friendships.

My father passed away a couple months into the building process. It was very unexpected and very difficult. Because we had to travel to the funeral, the people in our group told us they would donate any hours we needed to cover our weekly hours. Our group was very generous and kind. We truly appreciated them. We know these families care about us. On the anniversary of our open house, we always have a get-together to celebrate. We love the families we built with!

Neighborhood Nonprofit Housing Corporation (NNHC): A Utah-based nonprofit committed to creating quality affordable housing opportunities in their communities and giving households skills necessary to become self-sufficient. NNHC offers programs such as mutual self-help housing, and housing and foreclosure counseling, and as well as loan products.

It has now been five years since Yvette was hired by FHP to work as the Family Construction Coordinator II. In her role, she has assisted 144 first time homeowners achieve their homeownership dreams. Yvette has educated self-help homebuyers about the building process, coordinated their schedules, inspected their work, motivated them to push forward and proudly provided them the keys to their new homes. With the homebuilding process taking 6 to 8 months to complete, Yvette plays an integral role in the future of each of the self-help home buying families. She has witnessed great struggles that some new self-help home buying families endure and overcome during the construction process which in turn re-motivates and re-inspires her.

It has now been five years since Yvette was hired by FHP to work as the Family Construction Coordinator II. In her role, she has assisted 144 first time homeowners achieve their homeownership dreams. Yvette has educated self-help homebuyers about the building process, coordinated their schedules, inspected their work, motivated them to push forward and proudly provided them the keys to their new homes. With the homebuilding process taking 6 to 8 months to complete, Yvette plays an integral role in the future of each of the self-help home buying families. She has witnessed great struggles that some new self-help home buying families endure and overcome during the construction process which in turn re-motivates and re-inspires her.

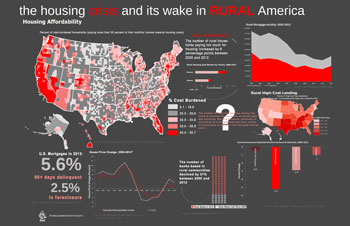

The housing crisis and its wake in rural America

The housing crisis and its wake in rural America